Visions of Rate Cuts Dancing In Their Heads

Visions of Rate Cuts Dancing In Their Heads

I am not a doctor, scientist, or expert in anything. This content should not be construed as advice or recommendation, but is intended for entertainment and informational purposes only.

Just like the children in the “The Night Before Christmas” all snuggled in their beds with visions of sugar plums dancing in their heads as they await the arrival of Santa Claus, investors are having visions of rate cuts dancing in their heads as they await the announcement from their version of Santa, Federal Reserve Chairman Jerome Powell.

We can see investor’s excitement in the action in the stock market. The Nasdaq, which had been falling since hitting a new all-time high almost a year ago to the day, began rallying in late January, but was starting to roll over in August as the hoped for rates cuts waned due to “sticky” inflation.

However, sentiment has quickly shifted and the most recent employment report, which was a case of bad news is good news for the market, and the most recent CPI report have investors absolutely giddy that Powell will ride in on his sleigh and soon begin delivering rate cuts they believe will support asset prices. The market has ripped higher in the last month, and is a whisker below its all-time highs.

Source: https://finance.yahoo.com/quote/NQ%3DF?p=NQ%253DF

The S&P 500 is showing similar action.

Source: https://finance.yahoo.com/quote/ES%3DF?p=ES%253DF

Could this be the beginning of a new stock market rally? Has the Fed pulled off the soft-landing, and now it’s up, up, and away from here?

Nobody can predict the future, especially the medium to longer-term future. Some people might get lucky, some more often than others, but nobody has a crystal ball. This rally could be for real and run on indefinitely, or it could be a massive head fake suckering more people in before it drops like a stone from a plane crushing retirement accounts.

I am one who has no clue how this is going to play out. I’m often wrong and always in doubt so I’ve given up on trying to guess where things will go. But I’m also not a buy and hold guy, at least not when it comes to paper assets like stock and bonds. It pays to protect against downside action that can decimate a portfolio.

For someone in their twenties, a market crash may not be a big deal assuming stocks always go higher which isn’t always the case. For someone in their middle years or in retirement, it can be downright devastating, especially if stocks don’t ultimately resume their upward march.

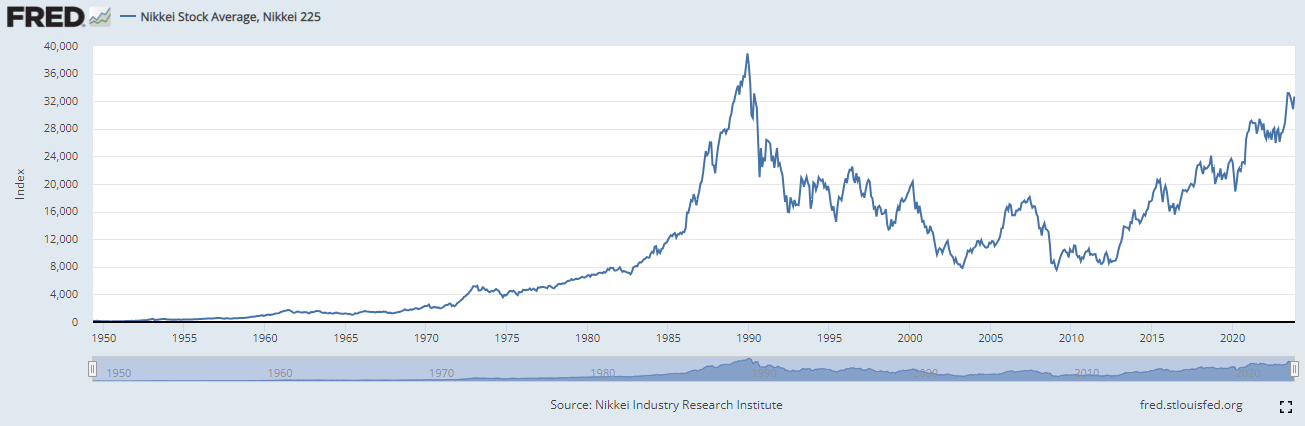

The Japanese Nikkei has still not returned to it’s all-time high in 1990 after decades of central bank quantitative easing!

Or how about the French CAC 40 index which did not recover its peak in the year 2000 until the governments engineered a global financial bailout in 2020? I know it’s just the Frenchies, but do you have 20 years to recover your losses?

Source: https://tradingeconomics.com/france/stock-market

Will this time be the same, or will it be different for us here in the U.S.? We suffer from recency bias and forget that stocks have taken years to recover in the U.S. as well, especially when adjusted for inflation. For example, the S&P 500 did not recover it’s all-time high in 1968 until 1992 on an inflation-adjusted basis. It took 16 years to recover after the Dot.com crash.

Source: https://www.macrotrends.net/2324/sp-500-historical-chart-data

Even though in nominal terms your portfolio was made whole much sooner, your purchasing power had been crushed and took a couple of decades to get you back to the same wealth status you enjoyed in prior years. This is the insidiousness of inflation, and is the big secret in the financial world. Always ask to see inflation-adjusted returns to evaluate the true performance of a financial product.

I find it highly unlikely that the Federal Reserve will actually pull off the much hyped “soft-landing.” The reasons for my doubt are multi-fold.

For one, the Federal Reserve has never pulled off a soft-landing, and I see no compelling reason why this time will be different. They have an atrocious record of predicting and responding to market conditions.

As well, it’s not readily apparent that the Federal Reserve has control over interest rates and monetary conditions the way the want people to believe they do, and in fact, there is plenty of evidence to suggest they have almost no control. Check out Jeff Snider’s Eurodollar University to learn more about that.

In addition, the yield curve is still significantly inverted indicating that all is far from well. When you can earn more by lending your money to Uncle Sam for 1 month than you can for 30 years, you know problems are brewing.

Source: https://home.treasury.gov/

Falling or low interest rates, especially longer-term rates, signal weakness in the economy not strength. If we had a rip roaring economy and rising inflation, we would see much higher interest rates on the long end of the curve.

Speaking of inflation, the October CPI report came in showing a resumption in the disinflation trend. This could accelerate to the downside which would not be a good thing unfortunately, especially if you loaded up with debt the past few years.

Speaking of debt, housing prices remain elevated, but there is more than meets the eye there too. Yes, inventories are tight, but new home sales, which are the big driver in housing prices currently, are kept artificially high by homebuilders offering massive interest rate buy downs to the tune of $50K+ so buyers can afford the monthly payments instead of lowering their prices.

They are doing this to offload inventory with hopes that interest rates drop suddenly and home prices begin to surge in the near future. This is not sustainable and eventually homebuilders will likely have to begin lowering prices which will have a downward effect on all home values.

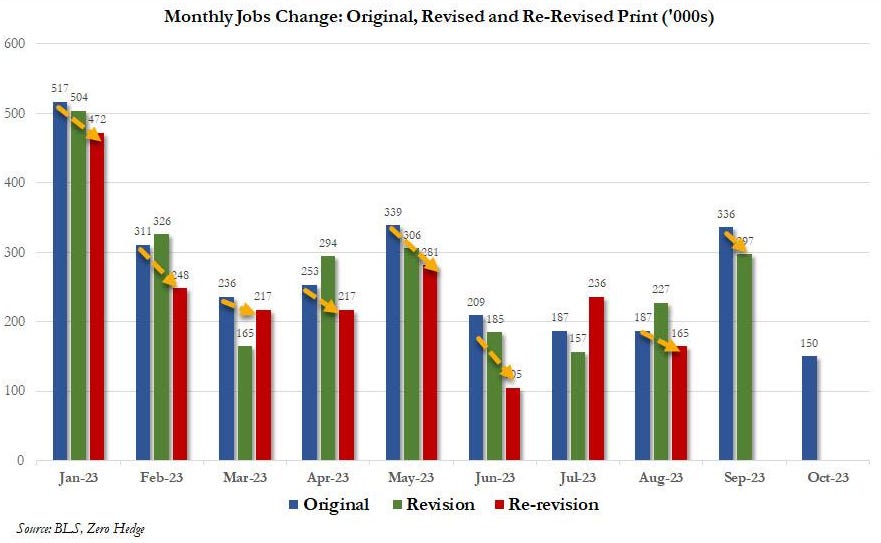

Employment is also weaker than the official numbers reveal, but even the alchemists at the BLS can’t hide the downward trend in employment. 8 of the last 10 months have been revised lower than originally reported, and September’s numbers are purely a statistical illusion that will likely be re-revised even lower.

Source: https://www.zerohedge.com/markets/record-number-multiple-jobholders-closer-looks-inside-horrific-october-jobs-report

The Household Survey, which I would consider far more accurate than the Establishment Survey because it’s actually completed by humans finding and losing jobs, tells a far more bleak story. There are a record number of multiple jobholders. Who really wants to work more than one job? Hell, who really wants to work one job?

As I’ve stated multiple times in these digital pages, I don’t make predictions and I’m often wrong. Nobody can time a crash with any real certainty. As the saying goes, the market can remain irrational longer than you and I can remain solvent.

I don’t offer advice or recommendations beyond suggesting you find ways to protect yourself to the downside and focus on real assets. If you’re going to play in the stock market or hang your financial future on assets that you hope will only appreciate forever into the future, you should ask yourself one question, “How much am I willing to lose and for how long?”